Prolonged Iran war may push copper price below $10 000/t, disrupt sulphuric acid supply

As war in the Middle East continues, a prolonged Iran war would squeeze the big-three copper miners' earnings before interest, taxes, depreciation and amortisation (Ebitda) more than consensus reflects, with Bloomberg Intelligence’s (BI's) scenario showing that Southern Copper faces a 20% cut, Antofagasta a 32% cut and First Quantum a 55% cut.

With this in mind, a report by BI global head of metals and mining Grant Sporre shows that oil of $150/bl-plus and curbed flows could drive copper below $10 000/t and result in a refined surplus of between 100 000 t to 200 000 t.

BI posits that the copper price could slip below $10 000/t if a protracted Iran war means Strait of Hormuz traffic remains limited, pushing oil above $150/bl.

In that scenario, waning global GDP points to copper-demand growth slowing to between 0.5% to 1% and refined copper staying in a 100 000-t to 200 000-t surplus.

Yet less worldwide oil dependence should prevent a full demand contraction, says BI.

Surpluses may be tempered by sulphur shortages in the Democratic Republic of Congo (DRC), which has the highest share of sulphuric-acid-based output globally, and relies heavily on Gulf supplies.

BI says a $10 000/t price may prove supportive as the minimum needed to incentivise new supply.

“A multimonth conflict looks less damaging, driving a balanced market and $10 500/t to $11 500/t pricing. A less-likely quick resolution would keep a deficit and price near $12 000/t.”

In another scenario, BI posits that a sustained Iran-linked oil shock – if the war drags on beyond a year and flows remain constrained through the Strait of Hormuz – would likely tip refined copper into a meaningful surplus and pull the price toward $10 000/t.

The recovery from the inflation boost after Russia's invasion of Ukraine is intact, but fragile, BI says, adding that an oil price above $150/bl would revive inflation and slow growth as central banks pause rate cuts or increase rates.

When oil briefly topped $120/bl in early 2022, BI notes, refined copper demand only rose by 1.5%, well below the 2.5% long-run trend.

“If growth slows to 1%, we see a 200 000-t to 350 000-t surplus in 2026/27.

“Sulphur shortages into the DRC – where about 50% to 60% of copper output depends on sulphuric acid – could cap the country's mine-supply growth, limiting the surplus to 100 000 t to 200 000 t.”

Further, BI argues that the scenario in which the Iran war continues for several months points to the refined-copper market ending 2026 about balanced, before moving into a modest surplus in 2027, pulling prices toward $11 000/t to $11 500/t.

BI notes that oil at $110/bl to $120/bl would stoke inflation risk and modestly dent global growth as the world's economy becomes less sensitive to the price of crude.

In that oil-price scenario, BI posits that copper demand is likely to edge up by between 1.5% and 2%.

“Yet the negative effect of sulphur shortages into the DRC would be more limited.

“The ramp-up of Ivanhoe-Zijin's smelter also provides a domestic source of sulphuric acid, easing the dependence on Gulf supply.”

Moreover, BI posits that the rapid rise of global inventories implies that the copper market is currently in surplus.

“Yet the recent price drop, combined with any quick resolution to the Iran war, points to demand rebounding and resulting in a small market deficit over the full year similar to the modest one in 2025.”

BI says it had anticipated slower global demand growth of between 2% to 2.3% this year as high prices hindered affordability.

“Yet the slow start to China's economic growth points to that being lower versus our earlier calculation.

“It may prove challenging to increase mined supply in 2026, when including a healthy 1.1-million-ton disruption allowance, as a series of stoppages at many of the world's biggest mines continues.

“That still leaves the global smelting industry scrambling for copper concentrate and scrap to match growth in demand.”

Meanwhile, BI indicates that consensus Ebitda for three of the largest copper miners still prices in a relatively quick resolution of the Iran war.

Yet, it notes that a prolonged scenario – assuming copper averages $10 000/t over 2026 and 2027 and unit cash costs increase by 10% to 20% for individual mines – suggests Antofagasta, First Quantum and Southern Copper's Ebitda could fall sharply – by an average of 36% this year and by 45% in 2027 – versus consensus.

Further, BI posits that a prolonged conflict would squeeze high-cost copper miners, echoing 2023 with 20%-plus cost inflation alongside a flat copper price versus 2024.

BI says lower-ore-grade cathode producers look most exposed owing to a reliance on sulphur and sulphuric-acid inputs and often lack gold by-product credits.

It adds that more competitive mines can offset costs with gold revenue. High-cost producers' profit margins might be able to reach about 40% in 2026, from roughly 70% in 2025, in this scenario.

On an all-in basis – cash costs plus royalties and sustaining capital expenditure (capex) – margin might compress to about 7%, near the long-run average that includes periods of negative margins in the 1980s and 1990s.

BI argues that that could result in sustaining capital and exploration cuts, while weaker cash flow would likely slow the project approvals needed to avoid a longer-term supply gap.

Moreover, BI points out that its China copper-demand proxy fell sharply in the fourth quarter, signaling a weaker first half demand outlook, while the market awaits the latest post-Lunar New Year data.

“We anticipate the government will support targeted measures in 2026 to ensure GDP goals are met, translating into demand growth of 0.5% to 1% this year, albeit significantly below 2025's 4% gain.”

There are also downside risks, the longer the Iran war drags on, BI warns.

It notes that the proxy fell to minus 5.7% in December, a multiyear low as the property market continues to exert a drag on copper's prospects, though declines in Chinese grid spending and appliance output – combined with slowing vehicle sales – point to waning demand.

BI says Bloomberg's China Financial Conditions Index has weakened across all subcomponents: credit availability, policy stance, external conditions, funding and market risk.

Gulf oil and shipping disruptions would likely tighten sulphur supply and lift sulphuric acid prices, steepening the copper cost curve and raising downside risk for solvent extraction and electrowinning (SX-EW) output in the DRC.

Though acid is usually a regional market, the Gulf is a major sulphur export hub – about 25% of global output – so disruption can transmit through higher delivered costs and, in some cases, shortages.

For Chilean openpit SX-EW, BI notes that acid can be between 20% to 25% of costs, based on Antofagasta's disclosure.

If prices return to 2022 levels – $255 a short ton, or 50% above today – BI says unit costs could rise by 10% to 13%.

“High-cost mines with limited byproduct credits are most exposed.

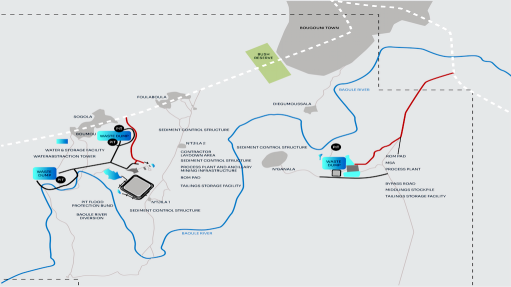

“In the DRC, SX-EW produced about 1.5-million tons of cathode in 2025 – 45% of output versus 15% globally – and relies on imported sulphur for primary acid.”

Further, BI says visible copper stocks have surged to about 1.4-million tons from roughly 440 000 t in late June 2025, signalling softer China demand and buyers delaying purchases in the fourth quarter after prices rose and off-exchange material surfaced.

BI says the speed of the build-up reduces the urgency for fabricators to chase units and caps a rally until inventories normalise.

Inventories pushing well above 800 000 t also suggest a market in surplus for now.

Including China's bonded-warehouse stocks, BI notes that global inventory sits near 18 demand days, above the 11-day average since 2013, yet below the prior 22-day peak.

The price dropping under $12 000/t might trigger restocking, though copper is likely to test sub-$10 000/t if the Middle East conflict drags on and caution keeps inventories rising toward the peak, says BI.

“As an example of a typical miner, Antofagasta's direct oil exposure looks manageable at $100/bl, yet broader inflation across key consumables is the bigger cost risk, partly cushioned by higher gold byproduct credits,” it notes.

BI adds that fuel and lubricants, with a clear link to oil were, 7% of the $2.38-a-pound 2025 gross cash cost.

Energy, mostly renewable, is another 12%, limiting oil pass-through.

If oil averages $100 – about 50% above last year – BI says it calculates a direct cost lift of about $0.09/lb, or 8%, versus 2025.

“A wider inflation scenario is more punitive – if most inputs rise 3% and sulphuric acid plus materials and spares jump 25%, the cost uplift is closer to 25c, or 21%, taking net cash cost to about $1.44/lb.

“Stronger gold prices could offset much of that, potentially holding the net cash cost increase to 5%.”

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

For over 15 years, Lilak Aluminium, a trusted leader in architectural extrusion supply, has delivered excellence to businesses like yours.

VISIT SHOWROOM

ISO-certified Condra manufactures overhead cranes, portal cranes, cantilever cranes and crane components: hoists, drives, end-carriages, brakes and...

VISIT SHOWROOM

Press Office

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation