PGMs, China’s stockpiling spur mining production leap, Minerals Council reports

JOHANNESBURG (miningweekly.com) – South Africa’s mining sector entered 2026 with robust momentum, posting notable year-on-year production gains in February largely on the back of platinum group metals (PGMs) and China’s stockpiling of key steelmaking inputs.

However, the sustainability of this growth is questionable as much of the expansion reflects base effects rather than a structural demand shift across mineral commodities, Minerals Council South Africa acting chief economist Bongani Motsa outlines in a media release to Mining Weekly.

Persistent contraction in coal highlights underlying weaknesses, with the industry facing multi‑month declines.

Following a stronger-than-anticipated start to 2026, mining sector production rose by 9.7% year-on-year, which builds on the 5% increase reported in January.

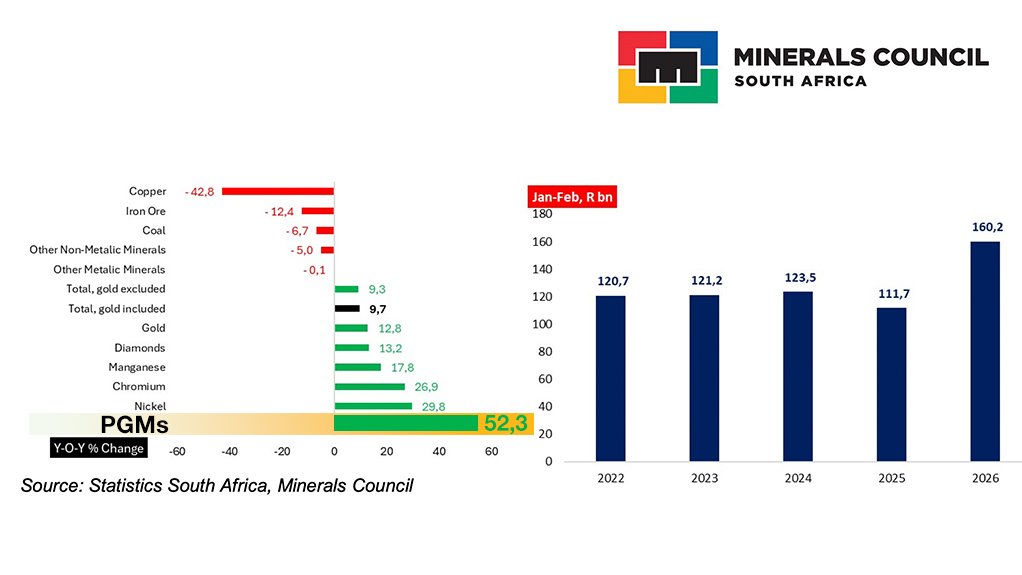

A detailed review of the data suggests that the growth was driven by the base effect of PGMs expanding by 52.3% and adding 9.4 percentage points to overall growth and also by stockpiling by China.

China has been actively accumulating reserves of critical steelmaking raw materials, including iron ore, chrome ore, and manganese ore. This strategy is motivated by concerns over supply security, heavy reliance on imports, and a desire to exert influence on global pricing. While iron ore production declined by 12.4%, chrome production grew by 26.9% and manganese production by 17.8%. Combined chrome and manganese contributed 4.1 percentage points to February’s growth number, Motsa adds.

PGMs alone accounted for 27.1% of the overall 49% growth of South Africa’s total production basket in February, when coal production was down 12.4% and iron ore production down 6.7%.

This was the fourth successive month of lower production for coal and the third contraction in four months for iron ore.

Mining production performance in the first quarter of 2026 is projected to grow by 1.3% quarter-on-quarter.

SALES SURGE

In February, total mineral sales surged by 58.3% year-on-year, rising from R49.6-billion in 2025 to R78.6-billion in 2026. This increase was driven primarily by strong performances in gold (+397% to R20-billion), PGMs (+132% to R23.1-billion), and chrome ore (+53.8% to R6-billion).

Year-to-date total mineral sales figures indicate a widening gap of R48.5-billion between January and February last year and the same period in 2026 – the difference between R160.2-billion and R111.7-billion. In the January commentary the difference was R20-billion in favour of higher sales in 2026.

Commodity prices for precious metals continued their upward trajectory, with rhodium recording the strongest price growth within the segment, further supporting overall mineral revenues. The rhodium price grew 135.4%, platinum by 118.8%, palladium by +78.4%, gold +73.3%, coal +0.5%, and iron ore -6.7%.

Persistent contraction in coal highlights underlying weaknesses, with the industry facing multi‑month declines.

LOOKING AHEAD

This year’s first-quarter production is projected to grow modestly at 1.3% quarter-on-quarter, suggesting that while headline figures remain positive, the sector’s near‑term outlook is tempered by uneven performance across commodities and continued reliance on external demand drivers.

The ongoing Middle East conflict involving the US, Israel, and Iran is expected to have direct and indirect impacts.

Directly, it will raise fuel costs, thereby impacting the sector’s profitability in 2026. For example, the sector typically spends, on average, R2.9-billion a month on petrol and diesel. As a result of the conflict, in April 2026, fuel expenditure is projected to rise to around R4-billion.

Indirectly, if the war continues, not only will it raise CPI inflation beyond the targeted mid-point of 3%, but interest rates will also ultimately have to increase.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Projects

Latest Multimedia

Latest News

Showroom

Sulzer South Africa, established in 1922, partners with critical industries like power, oil & gas, water, mining, and chemicals to boost...

VISIT SHOWROOM

CMTS is a leading, well-established EC&I contractor with 37+ years of mining and industrial experience. We execute full-scope EC&I projects with...

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation